Loan into Equity

✨ Introduction

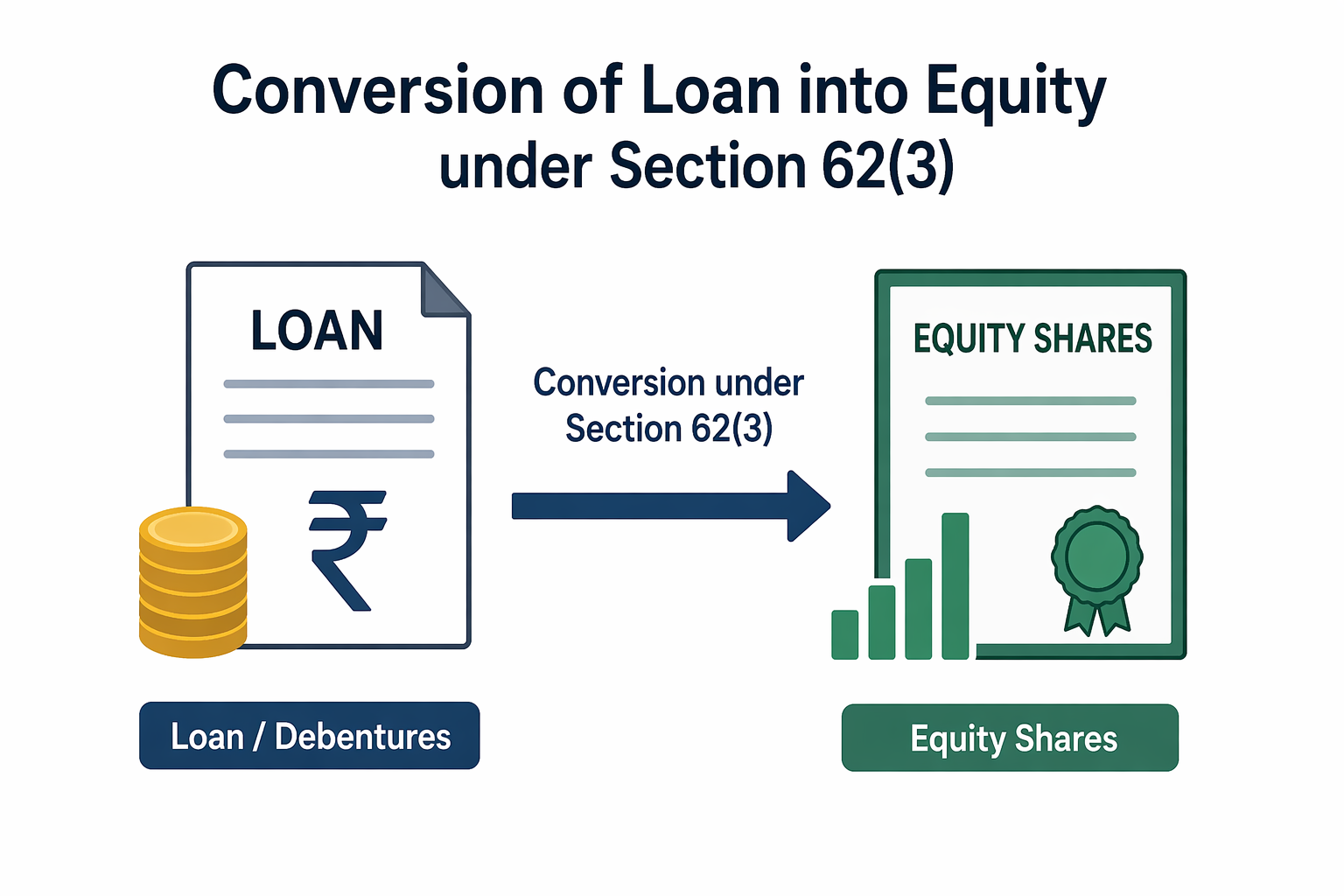

In the corporate world, companies often raise funds through loans or debentures. However, instead of repaying such liabilities in cash, companies may convert them into equity shares.

This conversion is legally permitted under Section 62(3) of the Companies Act, 2013, subject to certain conditions.

This provision is highly useful for:

- Startups facing cash flow issues

- Companies restructuring debt

- Investors seeking equity participation

In this article, we will cover complete provisions, conditions, and step-by-step procedure for conversion of loan/debentures into equity shares.

📜 Legal Provision – Section 62(3)

As per Section 62(3) of the Companies Act, 2013:

(3) Nothing in this section shall apply to the increase of the subscribed capital of a company caused by the exercise of an option as a term attached to the debentures issued or loan raised by the company to convert such debentures or loans into shares in the company:

Provided that the terms of issue of such debentures or loan containing such an option have been approved before the issue of such debentures or the raising of loan by a special resolution passed by the company in general meeting.

⚖️ Key Elements of Section 62(3)

1. Conversion must be pre-approved

- The loan agreement / debenture terms must contain a conversion clause.

2. Special Resolution is mandatory

- Shareholders must approve the conversion terms by passing a Special Resolution.

3. Terms must be predefined

🔍 Important Clarification (Practical Understanding)

👉 Section 62(3) is an exception to Section 62(1)(c) (Preferential Allotment)

Meaning:

- If conversion clause already exists

- Special Resolution already passed at the time of borrowing

- Then Section 42 (Private Placement) may not apply

👉 Compliance becomes simpler compared to fresh preferential allotment

🧾 Conditions for Valid Conversion

For a valid conversion under Section 62(3), the following must be ensured:

- Conversion clause exists in agreement ✅

- Special Resolution passed at the time of borrowing ✅

- Articles of Association authorize such issue ✅

- Terms are clearly defined ✅

- Proper Board approval at time of allotment ✅

📝 Step-by-Step Procedure

✅ STEP 1: Verify Conversion Terms

- Check loan agreement / debenture deed

- Ensure:

- Conversion clause exists

- Terms are clear

- Special Resolution already passed

✅ STEP 2: Check Articles of Association (AOA)

- If not authorized → alter AOA first

✅ STEP 3: Board Meeting (for Conversion)

Pass Board Resolution for:

- Approving conversion of loan into equity

- Approving allotment of shares

✅ STEP 4: Allotment of Shares

- Allot shares as per agreed conversion terms

✅ STEP 5: File Form PAS-3

- File Return of Allotment within 30 days

- Attach:

- List of allottees

- Board Resolution

✅ STEP 6: Issue Share Certificates

- Within 2 months of allotment

✅ STEP 7: Update Statutory Registers

- Register of Members

- Shareholding pattern

📊 Documents Required

- Loan Agreement / Debenture Trust Deed

- Special Resolution copy

- Board Resolution

- PAS-3 attachments

- Updated AOA (if amended)

💡 Advantages of Conversion

- Reduces debt burden

- Improves debt-equity ratio

- No immediate cash outflow

- Strengthens company’s net worth

🏁 Conclusion

Conversion of loan or debentures into equity under Section 62(3) is a powerful compliance tool for companies.

If executed properly, it helps in:

- Financial restructuring

- Compliance simplification

- Long-term capital strengthening

However, strict adherence to legal provisions and proper documentation is essential to avoid ROC objections.

📞 CTA – LegalGlobe

Want to Convert Loan into Equity without ROC Queries?

Get expert assistance for:

- Drafting agreements with conversion clause

- Board & shareholder resolutions

- ROC filings (PAS-3, MGT-14)

👉 Contact LegalGlobe for professional compliance support.

❓ Frequently Asked Questions (FAQs)

1. What is Section 62(3) of the Companies Act, 2013?

Section 62(3) allows a company to convert its loan or debentures into equity shares if such conversion is already provided in the terms of issue and approved by shareholders through a special resolution.

2. Is it mandatory to pass Special Resolution at the time of conversion?

👉 No, Special Resolution is not required at the time of conversion

👉 However, Special Resolution must have been passed at the time of availing the loan or issuing debentures, approving the conversion terms.

👉 If such prior approval does not exist:

❌ Conversion cannot be done under Section 62(3)

👉 Company must follow:

- Section 42 (Private Placement)

- Section 62(1)(c) (Preferential Allotment)

3. Is Section 42 (Private Placement) applicable in case of conversion under Section 62(3)?

👉 Generally, Section 42 does not apply if:

- Conversion clause already exists

- Terms were approved earlier

👉 Because Section 62(3) acts as an exception to preferential allotment provisions

4. Whether valuation report is required for conversion?

- Law me explicitly mention nahi hai under 62(3)

- But practically, valuation report recommended hai (especially related party or scrutiny cases me)

5. Can a company convert unsecured loan into equity shares?

✅ Yes, allowed

Provided:

- Conversion clause exists

- Special Resolution passed

- Terms clearly defined

6. What forms are required to be filed with ROC?

- PAS-3 (Return of Allotment) – Mandatory

- MGT-14 – Only if Special Resolution is passed (earlier or fresh)

7. What is the time limit for filing PAS-3?

PAS-3 must be filed within 30 days from the date of allotment of shares.

8. Is alteration of AOA required for conversion?

👉 Yes, if AOA does not permit:

- Issue of shares

- Conversion of loan/debentures

👉 Then AOA must be altered before conversion

9. What happens if conversion clause is not present in the agreement?

❌ Section 62(3) cannot be applied

👉 In such case:

- Company must follow Section 62(1)(c) (Preferential Allotment)

- Along with Section 42 compliance

10. Can conversion be done partially?

✅ Yes, partial conversion is allowed

- As per agreed terms

- Remaining loan can continue

11. Is GST applicable on conversion of loan into equity?

❌ No, GST is not applicable

👉 Because it is not a supply of goods or services

12. Whether TDS is applicable on such conversion?

👉 Generally, no TDS

But depends on:

- Nature of transaction

- Interest component (if any)

13. Can conversion be done at any time?

👉 Only as per terms defined in agreement

- If timeline mentioned → follow that

- If flexible → can be done mutually

14. Is share certificate required after conversion?

✅ Yes

- Must be issued within 2 months from allotment

15. What are the consequences of non-compliance?

- ROC penalties

- Allotment may be questioned

- Future funding issues

- Legal complications

🏁 Conclusion

Conversion of loan or debentures into equity under Section 62(3) is a powerful compliance tool for companies.

If executed properly, it helps in:

- Financial restructuring

- Compliance simplification

- Long-term capital strengthening

However, strict adherence to legal provisions and proper documentation is essential to avoid ROC objections.